Yez 13a44

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 3l3c15

Overview 3z723u

& View Yez as PDF for free.

More details 2i4a6q

- Words: 234

- Pages: 1

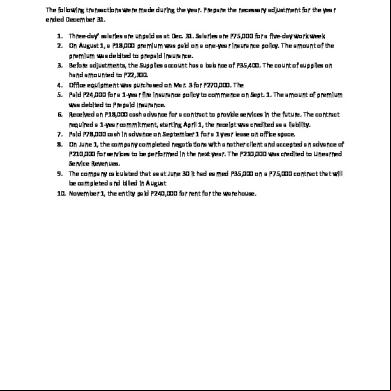

Adjusting Entries: The following transactions were made during the year. Prepare the necessary adjustment for the year ended December 31. 1. Three-day’ salaries are unpaid as at Dec. 31. Salaries are P75,000 for a five-day work week 2. On August 1, a P18,000 was paid on a one-year insurance policy. The amount of the was debited to prepaid insurance. 3. Before adjustments, the Supplies has a balance of P35,400. The count of supplies on hand amounted to P22,300. 4. Office equipment was purchased on Mar. 3 for P270,000. The 5. Paid P24,000 for a 1-year fire insurance policy to commence on Sept. 1. The amount of was debited to Prepaid Insurance. 6. Received an P18,000 cash advance for a contract to provide services in the future. The contract required a 1-year commitment, starting April 1, the receipt was credited as a liability. 7. Paid P78,000 cash in advance on September 1 for a 1 year lease on office space. 8. On June 1, the company completed negotiations with another client and accepted an advance of P210,000 for services to be performed in the next year. The P210,000 was credited to Unearned Service Revenues. 9. The company calculated that as at June 30 it had earned P35,000 on a P75,000 contract that will be completed and billed in August 10. November 1, the entity paid P240,000 for rent for the warehouse.

Related Documents g842

Yez 13a44

February 2023 0More Documents from "Rhouie Resubal" 2j4h2f